AI IPO Watch · ETF Mechanics

What Happens When the Same Company Becomes Easier to Buy in the U.S.?

SK Hynix now has a U.S. ticker. The reflex take is "ETFs will rotate into $SKHY." The real answer: ETFs do not automatically have to sell the Seoul line and buy the ADR. It depends on index rules, listing eligibility, liquidity, tax and custody setup — and whether the ADR becomes the preferred tradable line.

The short answer

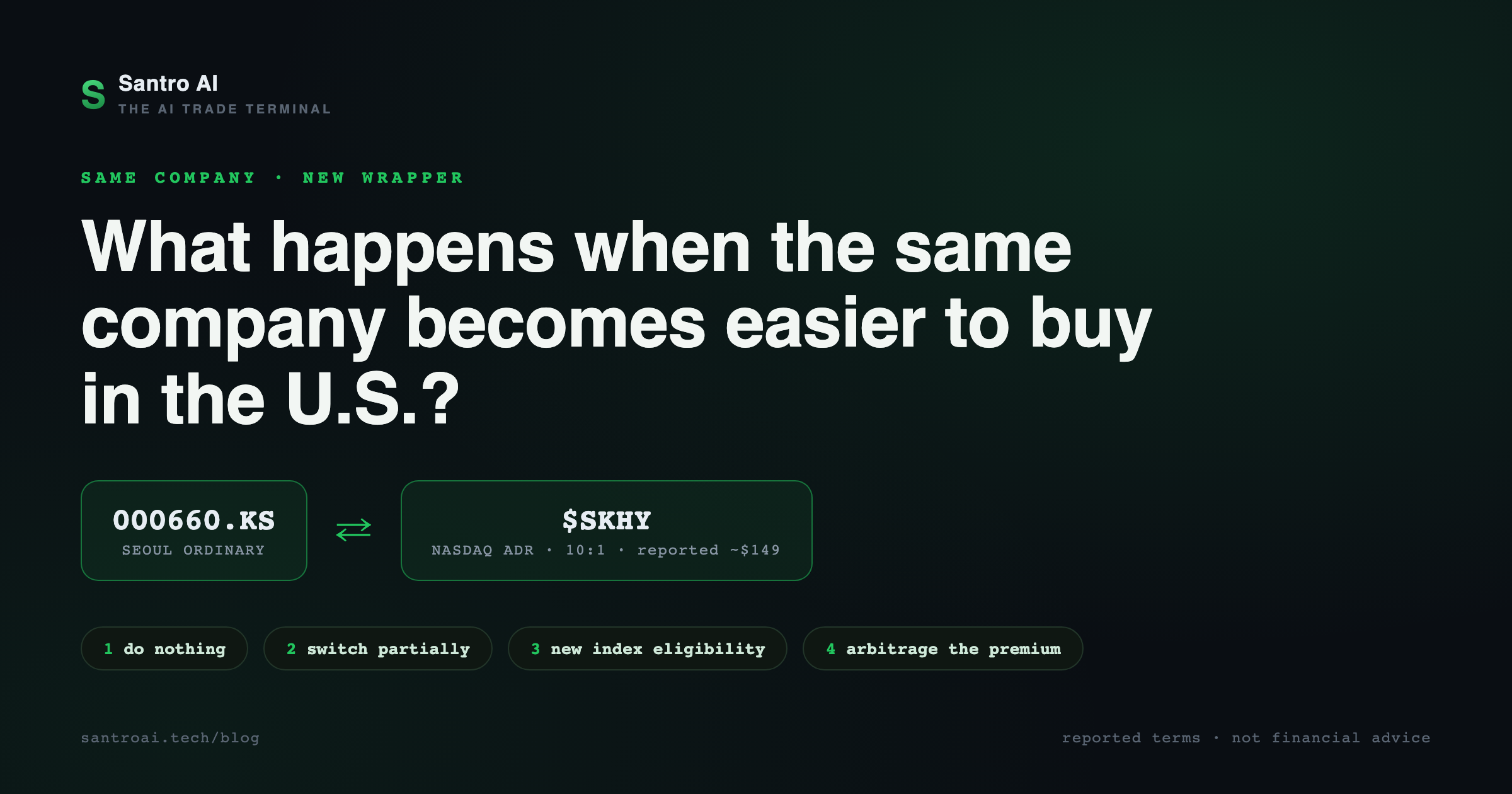

An ADR is a depositary wrapper over the same economic company. Funds that hold Seoul-listed SK Hynix (000660.KS) are not forced to do anything when $SKHY starts trading. What the new line changes is optionality — and there are exactly four ways that optionality can turn into flows.

1. "Do nothing" — the base case for Korea / EM / global index funds

Funds tracking Korea or emerging-market benchmarks will most likely keep the Seoul-listed ordinary shares. Their index owns the local Korean line; the ADR is just a wrapper. For country and region exposure, the local share is usually the clean benchmark instrument — a Korea ETF wants Korean-market exposure, not "U.S.-listed wrappers of Korean companies."

2. "Switch partially" — possible for thematic and active funds

Thematic products — memory, AI infrastructure, semiconductors, AI supply chain — can choose whichever line is easier to trade. If $SKHY becomes more liquid in U.S. hours, some funds may prefer it for execution, custody, and U.S. investor reporting.

This is where $DRAM gets interesting. Roundhill's memory ETF already gave U.S. investors packaged exposure to SK Hynix, Samsung, Micron and the storage names — Reuters described it as access to hard-to-reach Korean memory names, and market coverage has noted SK Hynix and Micron among its major holdings. The ADR makes the SK Hynix leg cleaner for U.S.-hours trading. Cleaner — not mandatory.

3. "Add as newly eligible" — the bigger one, for U.S. semiconductor indexes

Some U.S. semiconductor indexes require U.S.-listed securities. Seoul-listed SK Hynix sat outside that investable universe; $SKHY may become eligible once liquidity and seasoning requirements are met. WSJ reporting flagged exactly this: the U.S. listing may help SK Hynix appeal to institutions restricted from buying non-U.S. securities, and could potentially support inclusion in semiconductor indexes like the Philadelphia Semiconductor Index.

That is where passive demand could eventually come from. But it is not automatic on day one — index rules, float, listing seasoning, and committee decisions all sit in between.

4. "Arbitrage / parity" — the immediate technical layer

ADRs are supposed to track the underlying local shares adjusted for ratio and FX. The reported terms: 10 ADRs = 1 common share, ~$149 per ADR — which WSJ put at roughly a reported ~3% premium to the Seoul line. If $SKHY trades rich, arbitrage pressure appears. If a premium persists, that tells you something real: U.S. investors are paying for access, liquidity, time zone, or mandate eligibility.

That premium/discount is the tape to watch.

The TSMC playbook

TSMC is the clean analogy. Some U.S.-listed semiconductor ETFs hold the $TSM ADR because it is U.S.-listed, liquid, and tradable in U.S. hours. Global and emerging-market ETFs often hold the Taiwan local shares, because that is the benchmark exposure. Same company. Different wrapper. Different fund rules.

- Korea / global index funds: probably keep local 000660.KS

- U.S. thematic semi funds: may use $SKHY if eligible and liquid

- Active funds: choose best execution and liquidity

- Retail: finally gets a clean U.S. ticker

What it means for the rest of the memory complex

$MU — the most sensitive

Before $SKHY, Micron was the cleanest U.S.-listed memory proxy. Now U.S. investors can buy the HBM leader directly — a potential headwind for Micron's "only easy memory trade" premium. But it is not automatically bearish: Reuters quoted investors saying the ADR could narrow SK Hynix's valuation gap with Micron and potentially support re-ratings across Korean memory names. The listing can reprice the whole complex higher if investors decide HBM scarcity deserves U.S.-style AI multiples.

$DRAM — less hidden, more crowded

The basket already packaged the memory trade before the ADR. Now its biggest story has its own U.S. ticker, so the ETF loses some "only way in" uniqueness. It still offers what a single ADR cannot: basket exposure across SK Hynix, Samsung, Micron and storage — attractive if you want the theme, not single-name risk.

$NVDA — supply-chain truth, not competition

Nvidia GPUs are only as useful as the memory supply around them. SK Hynix being easier to buy makes the market more aware that the AI stack is not just GPU silicon — it is HBM, advanced packaging, EUV, capacity and delivery. Reuters reported Jensen Huang called SK Hynix Nvidia's largest partner and said the memory shortage could persist for years.

$WDC / $STX / $SNDK — dispersion risk

If the listing works, memory and storage sentiment can stay bid. But if $SKHY becomes the direct institutional "quality HBM" trade, lower-quality storage names may stop moving just because "memory good." Watch for the complex to stop trading as one block.

$SMH and the semi ETFs — later, maybe

If $SKHY becomes eligible for more semiconductor indexes, that creates passive demand — but not on day one. Index rules, liquidity, float, seasoning, and committee decisions matter. Until then, $SMH exposure to this story runs through the names it already holds.

The real question

The ADR does not change what SK Hynix earns. It changes who can own it, in which wrapper, at what hours, under which mandate. Flows follow rules, not headlines — and the first honest signal will be whether the ADR premium persists. Watch the memory & hardware sector heat and the $SKHY IPO watch profile as it seasons.

All deal terms (10 ADRs = 1 common share, ~$149/ADR, the ~3% premium to the Seoul close) and index-inclusion possibilities in this piece are reported from financial media (Reuters, WSJ, Barron's) and remain subject to change; index eligibility is speculative until an index committee acts. SK Hynix, Roundhill, and the index providers are not affiliated with Santro AI. Quotes shown elsewhere on the site are delayed ~15 min. Hot means attention, not direction. Not financial advice.